Last post, we show how to pull the latest options chain data from Yahoo Finance in Python using yfinance. Now we’re going to turn that raw data into powerful options indicators—think Put/Call Open‑Interest ratios, Volume / Open‑Interest spikes, and more—that can fuel real‑time alerts and reveal large‑trader positioning and whale activity.

Need custom metrics integrated into your options strategy? From the classic Put / Call ratio to bespoke indicators you define yourself, we’ll walk through all the Python code you need to get started with integrating custom indicators to get an edge in options trading.

For those that are totally new to Python you can follow step-by-step guide to getting setup here. Also for those that are interested in checking out making your own Discord server for options signal, this post may be of interest.

📋 Contents

Getting Options Data to Calculate Unusual Activity Metrics

In the last post we used Tesla to get options data, this time we will change it up a bit and get Apple options data and calculate some indicators. Note here we add two derived columns one for the put/call and the other for the expiry, this will be useful for using pandas groupby to calculate our indicators.

import pandas as pd

import yfinance as yf

# Initialize ticker

ticker = yf.Ticker("AAPL")

# Collect all chains

all_chains = []

for expiry in ticker.options:

chain = ticker.option_chain(expiry)

# tag each row with its expiry date

calls = chain.calls.copy().assign(expiry=expiry, side="call")

puts = chain.puts.copy().assign(expiry=expiry, side="put")

all_chains.extend([calls, puts])

# concatenate into one DataFrame

options_df = pd.concat(all_chains, ignore_index=True)

# optional: reorder columns so expiry/side come first

cols = ["expiry", "side"] + [c for c in options_df.columns if c not in ("expiry", "side")]

options_df = options_df[cols]

print(options_df.head())

'''

expiry side contractSymbol lastTradeDate strike \

0 2025-04-25 call AAPL250425C00100000 2025-04-16 16:50:54+00:00 100.0

1 2025-04-25 call AAPL250425C00110000 2025-04-21 16:31:25+00:00 110.0

2 2025-04-25 call AAPL250425C00120000 2025-04-21 16:31:25+00:00 120.0

3 2025-04-25 call AAPL250425C00125000 2025-04-17 18:38:53+00:00 125.0

4 2025-04-25 call AAPL250425C00126000 2025-04-17 14:56:35+00:00 126.0

lastPrice bid ask change percentChange volume openInterest \

0 97.30 92.10 93.55 0.000000 0.000000 10.0 18

1 81.42 82.15 83.55 -2.240006 -2.677511 2.0 19

2 71.45 72.15 73.60 -10.750000 -13.077859 2.0 65

3 73.45 67.15 68.65 0.000000 0.000000 2.0 32

4 70.13 66.15 67.70 0.000000 0.000000 4.0 7

'''

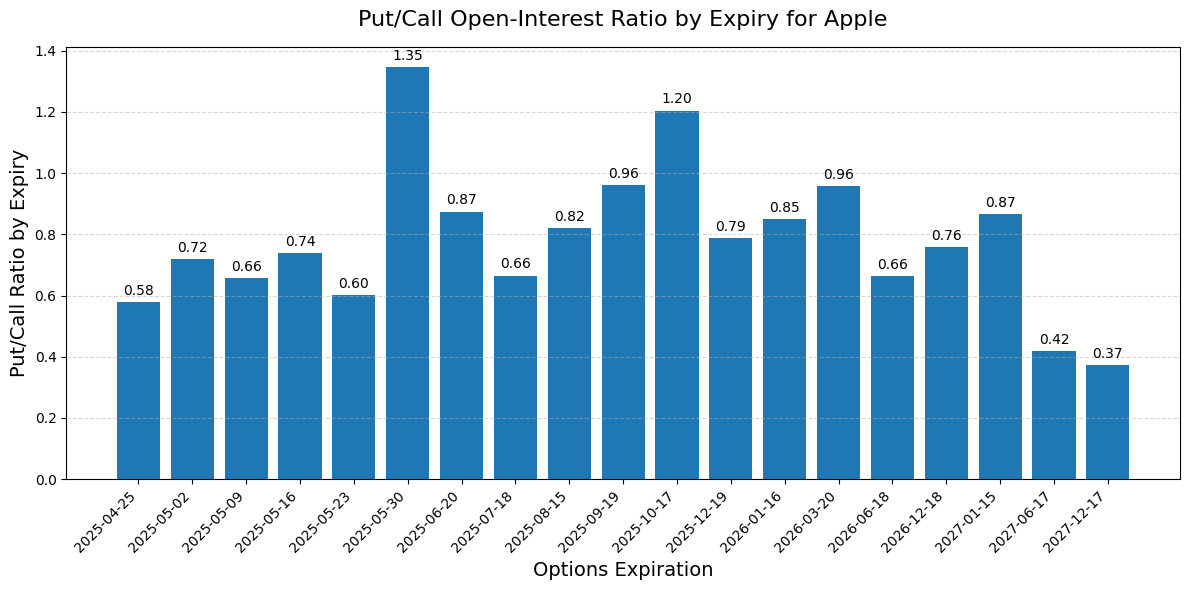

Put / Call Ratio

What is the Put Call Ratio?

The Put / Call Open‑Interest Ratio is shown by the formula below. It is calculated by taking the sum of put option open interest and dividing by sum of call open interest.

\([ \mathrm{PCR}_{\mathrm{OI}} \;=\; \frac{\displaystyle\sum \mathrm{OI}_{\text{puts}}} {\displaystyle\sum \mathrm{OI}_{\text{calls}}} ]\)

The Put/Call ratio is widely used to gauge trader sentiment, higher values indicating increased levels of fear in the market

PCR > 1 suggests bearish sentiment (more puts outstanding than calls)

PCR < 1 suggests bullish sentiment (more calls outstanding than puts)

Python Code to Calculate Put Call Ratio ⬇️

# groupby expiry

oi_by_side = (

options_df

.groupby(['expiry', 'side'])['openInterest']

.sum()

.unstack('side')

)

# calculate the Put/Call Ratio

oi_by_side['PCR_OI'] = oi_by_side['put'] / oi_by_side['call']

oi_by_side.index = pd.to_datetime(oi_by_side.index)

oi_by_side = oi_by_side.sort_index()

print(oi_by_side[['call', 'put', 'PCR_OI']])

'''

ide call put PCR_OI

expiry

2025-04-25 262740 151940 0.578290

2025-05-02 88577 63672 0.718832

2025-05-09 34851 22894 0.656911

2025-05-16 266811 197127 0.738826

2025-05-23 15218 9173 0.602773

2025-05-30 6269 8436 1.345669

'''

Plot Put call Ratio

labels = oi_by_side.index.strftime('%Y-%m-%d')

fig, ax = plt.subplots(figsize=(12, 6))

bars = ax.bar(labels, oi_by_side['PCR_OI'])

ax.set_title('Put/Call Open‑Interest Ratio by Expiry for Apple', fontsize=16, pad=15)

ax.set_xlabel('Options Expiration', fontsize=14)

ax.set_ylabel('Put/Call Ratio by Expiry', fontsize=14)

ax.grid(axis='y', linestyle='--', alpha=0.5)

plt.xticks(rotation=45, ha='right')

for bar in bars:

height = bar.get_height()

ax.annotate(f'{height:.2f}',

xy=(bar.get_x() + bar.get_width() / 2, height),

xytext=(0, 3), # 3 points vertical offset

textcoords='offset points',

ha='center', va='bottom',

fontsize=10)

plt.tight_layout()

plt.show()

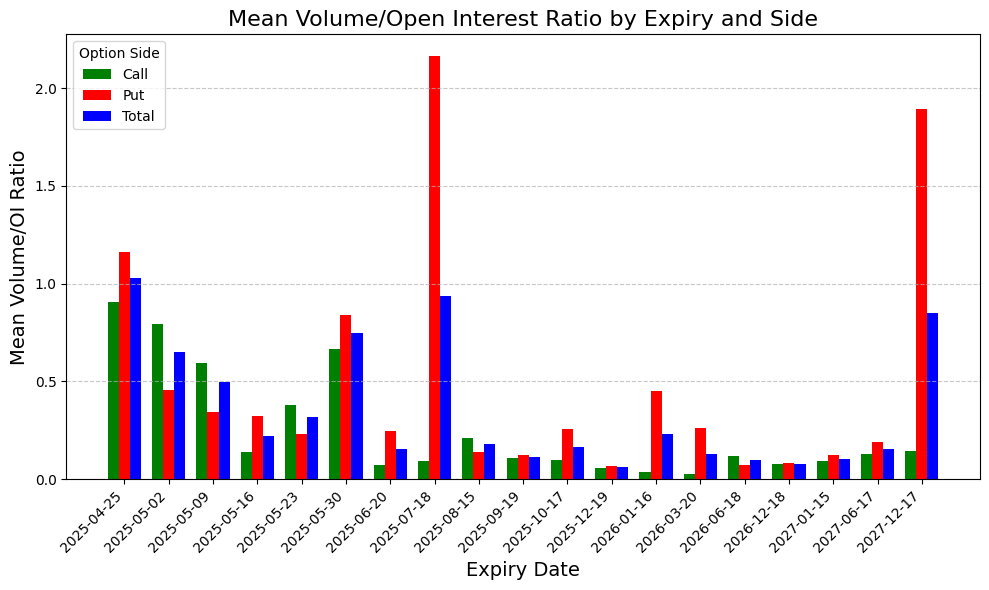

Unusual Activity: Volume Spike vs. Open Interest

What is Unusual Activity and Vol / OI Ratio

“Unusual options activity” refers to trading patterns that stand out from the norm—typically characterized by spikes in volume, sudden changes in implied volatility, or large block trades. Among these signals, the volume‑to‑open interest (Volume/OI) ratio is one of the simplest and most powerful metrics for spotting fresh positioning in the market.

A high Volume/OI ratio tells you that today’s trading activity is large relative to the number of contracts already outstanding, often flagging large directional bets or hedges before major events.

\([ \mathrm{vol\_to\_oi}_i \;=\; \frac{\mathrm{volume}_i}{\mathrm{openInterest}_i} \quad(\text{where }\mathrm{openInterest}_i>0) ]\)

Python code to Calculate Volume / OI Indicator

import pandas as pd

import numpy as np

# calculate the volume / OI ratio per contract

options_df['vol_to_oi'] = np.where(

options_df['openInterest'] > 0,

options_df['volume'] / options_df['openInterest'],

np.nan

)

#group by expiry & side

ratio_by_side = (

options_df

.groupby(['expiry', 'side'])['vol_to_oi']

.mean()

.unstack(level='side')

)

# calc the total (across both calls and puts) per expiry

total_ratio = (

options_df

.groupby('expiry')['vol_to_oi']

.mean()

.rename("total")

)

# combine

ratio_summary = pd.concat([ratio_by_side, total_ratio], axis=1).sort_index()

print(ratio_summary)

'''

call put total

expiry

2025-04-25 0.907152 1.161929 1.027628

2025-05-02 0.792265 0.456009 0.649260

2025-05-09 0.591911 0.344745 0.495996

2025-05-16 0.139945 0.320714 0.219031

2025-05-23 0.380570 0.229420 0.317591

'''

Plot Results to Identity Unusual Activity

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

ratio_summary.index = pd.to_datetime(ratio_summary.index)

x = np.arange(len(ratio_summary.index))

width = 0.25

# plot unsual options activity

fig, ax = plt.subplots(figsize=(10, 6))

ax.bar(x - width, ratio_summary['call'], width, label='Call', color='green')

ax.bar(x, ratio_summary['put'], width, label='Put', color='red')

ax.bar(x + width, ratio_summary['total'], width, label='Total',color='blue')

ax.set_title('Mean Volume/Open Interest Ratio by Expiry and Side', fontsize=16)

ax.set_xlabel('Expiry Date', fontsize=14)

ax.set_ylabel('Mean Volume/OI Ratio', fontsize=14)

ax.set_xticks(x)

ax.set_xticklabels(

ratio_summary.index.strftime('%Y-%m-%d'),

rotation=45, ha='right'

)

ax.legend(title='Option Side')

ax.grid(axis='y', linestyle='--', alpha=0.7)

plt.tight_layout()

plt.show()

From the plot above we can see that there is some unusual put activity for both the July 2025 & Dec 2027 Contracts, possibly signaling worries about downside volatility in the stock.

📚 Further Reading

- 🔗 Learn to Make Python Dashboards to Integrate This code

- 🔗 Get started with Python FastAPI

- 🔗 Completely New To Python Beginner Setup