Are you looking to take your cryptocurrency trading to the next level? Look no further than Bybit, the leading crypto derivatives exchange. With advanced trading tools, low fees, and a user-friendly platform, Bybit makes it easy to trade Bitcoin, Ethereum, and other popular cryptocurrencies. And if you sign up using our affiliate link through Codearmo and use the referral code CODEARMO, you'll receive exclusive benefits and bonuses up to $30,000 to help you get started. Don't miss out on this opportunity to join one of the fastest-growing communities in crypto trading. Sign up for Bybit today and start trading like a pro!

Users who sign up through the referal link above will also get access to a members only Discord group to ask questions and talk strategies and deployment.

What is Delta?

The delta of an option is a measure of the sensitivity of the option's price to changes in the price of the underlying asset. It quantifies the degree to which the option price is expected to change in response to a $1 change in the price of the underlying asset.

The delta value of an option can range between 0 and 1 for call options and between 0 and -1 for put options. Here's what the delta values indicate:

-

Call Options:

- Delta values for call options range from 0 to 1.

- A delta of 0 indicates that the call option's price is not affected by changes in the underlying asset's price.

- A delta of 1 indicates that the call option's price moves in lockstep with the underlying asset's price. For every $1 increase in the underlying asset's price, the call option's price is expected to increase by the delta value.

- Delta values between 0 and 1 indicate that the call option's price will increase, but to a lesser extent than the underlying asset's price increase. For example, a delta of 0.5 means the call option's price is expected to increase by $0.50 for a $1 increase in the underlying asset's price.

-

Put Options:

- Delta values for put options range from 0 to -1.

- A delta of 0 indicates that the put option's price is not affected by changes in the underlying asset's price.

- A delta of -1 indicates that the put option's price moves inversely with the underlying asset's price. For every $1 decrease in the underlying asset's price, the put option's price is expected to increase by the absolute value of the delta.

- Delta values between 0 and -1 indicate that the put option's price will increase, but to a lesser extent than the underlying asset's price decrease. For example, a delta of -0.5 means the put option's price is expected to increase by $0.50 for a $1 decrease in the underlying asset's price.

The delta of an option is a dynamic value that can change as the price of the underlying asset, time to expiration, and other factors fluctuate. It is an important parameter used in options pricing models and risk management strategies, such as delta hedging.

The latest deltas for Bitcoin and ETH options can be found on the third column from the left/right for puts and calls respectively on the option chain.

What is Delta Hedging?

Delta hedging is a risk management strategy used by traders and investors to offset the directional risk (price movement) of an option position by taking an opposing position in the underlying asset. It involves adjusting the portfolio's position in the underlying asset to maintain a neutral or zero overall delta.

Delta is a measure of the sensitivity of an option's price to changes in the price of the underlying asset. It represents the change in the option price for a $1 change in the underlying asset's price. Delta can be positive for call options and negative for put options.

Delta Hedging Call Example

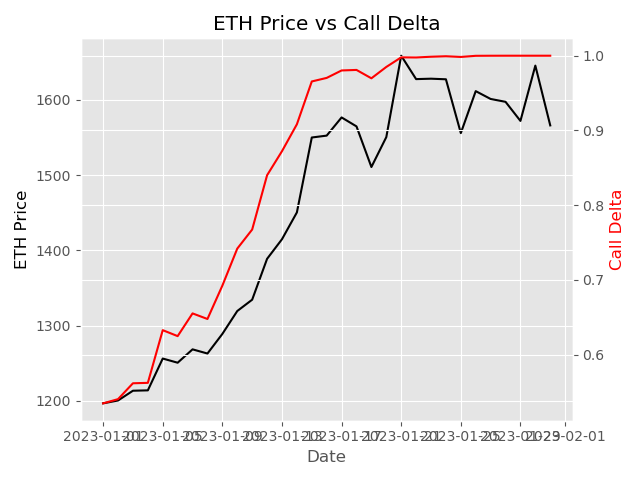

Lets say a trader bought a call option on ETH on the 1st January 2023 , note the following information:

1) ETH was priced at $1997 at the time of opening the trade

2) A call option with 1200 strike is currently trading at 94.20 USDC

3) The option expires 31st Jan 2023

4) Implied Volatility of the option is 70%

5) 0.534687 is the delta.

So let's take a look at the price of ETH and the options Delta over the course of January 2023.

As can be seen from the plot above, the delta of a call option is positively correlated with the price of ETH, this means that the more the price of the underlying asset goes up above the strike price of the option, the closer the delta of a call option will become to 1.

It is also worth noting that the delta of a call will rapidly approach 1 or 0 as we get towards expiration. This represents being in the money / above the strike , delta approaches 1 compared with out of the money /below strike , delta approaches 0 as we move towards the expiration date.

We can hedge this delta by taking an offsetting position in the ETH future. Since we have a starting delta value of approx 0.535 and assuming we want to set our portfolio delta value to zero, this would require an offsetting position of 0.535 * 1997 which gives us a short position of approximately $630 worth of ETH. The table below shows a few days of the PNL of both the option and the future, alongside a combined column.

| Timestamp | ETH Price | Hedge Value | Call Value | Option PNL | Future PNL | Combined |

|---|---|---|---|---|---|---|

| 1/1/2023 | 1196.8 | 639.913301 | 94.19307647 | 0 | 0 | 0 |

| 1/2/2023 | 1200.6 | 641.9451113 | 94.62956587 | 0.436489399 | -2.031810281 | -1.595320881 |

| 1/3/2023 | 1213.55 | 648.8693069 | 100.124599 | 5.931522504 | -8.956005842 | -3.024483338 |

| 1/4/2023 | 1214.05 | 649.1366503 | 98.73413329 | 4.541056812 | -9.2233493 | -4.682292488 |

| 1/5/2023 | 1256.3 | 671.7271725 | 122.2849161 | 28.09183965 | -31.8138715 | -3.72203185 |

| 1/6/2023 | 1250.75 | 668.7596601 | 117.076718 | 22.88364155 | -28.84635912 | -5.962717564 |

| 1/7/2023 | 1268.5 | 678.2503529 | 126.6901877 | 32.49711125 | -38.33705187 | -5.839940619 |

| 1/8/2023 | 1262.95 | 675.2828405 | 121.3058689 | 27.11279244 | -35.36953949 | -8.256747052 |

| 1/9/2023 | 1289 | 689.2114347 | 136.9766657 | 42.78358921 | -49.29813365 | -6.514544445 |

The animation below shows the evolution of the columns above over the life of the option.

It is worth noting that the trader made less PNL than he would have done if he did not delta hedge this position.

Delta Hedging Put Example

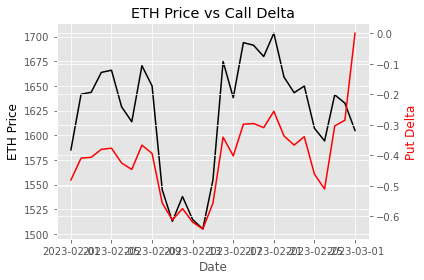

The same trader from above, now decides on the 1st Feb 2023 , that he wants to take a short position via a put option on ETH. Take note of the following information.

1) ETH was priced at $1585 at the time of opening the trade

2) A call option with 1600 strike is currently trading at 130.58 USDC

3) The option expires 1stth March 2023

4) Implied Volatility of the option is 70%

5) -0.481 is the delta.

Since the delta of the option is negative, in order to delta hedge the trader should take a long position in ETH i.e. Buy 0.481 ETH worth of the future.

Notice that towards the end of the life of the option the delta of the put option approaches 0 representing it finished out of the money, if the option was in the money i.e. ETH price less than Strike price, then the delta would have approached -1 as expiry draws nearer.

| timestamp | ETH Price | hedge_value | put_value | option_pnl | future_pnl | combined |

|---|---|---|---|---|---|---|

| 2/1/2023 | 1585.09 | 761.7829954 | 130.5830569 | 0 | 0 | 0 |

| 2/2/2023 | 1641.56 | 788.9220763 | 103.2469058 | -27.33615104 | 27.1390809 | -0.197070134 |

| 2/3/2023 | 1643.57 | 789.888068 | 100.1580919 | -30.424965 | 28.10507263 | -2.319892377 |

| 2/4/2023 | 1663.75 | 799.5864327 | 89.9153083 | -40.66774857 | 37.80343729 | -2.864311275 |

| 2/5/2023 | 1665.96 | 800.648543 | 86.73596253 | -43.84709434 | 38.86554759 | -4.981546747 |

| 2/6/2023 | 1628.76 | 782.7704872 | 99.22347489 | -31.35958198 | 20.98749182 | -10.37209016 |

| 2/7/2023 | 1613.69 | 775.5279522 | 103.3202859 | -27.26277096 | 13.74495686 | -13.5178141 |

| 2/8/2023 | 1670.57 | 802.8640762 | 77.71040165 | -52.87265522 | 41.08108085 | -11.79157437 |

| 2/9/2023 | 1649.95 | 792.9542507 | 82.98798133 | -47.59507554 | 31.17125531 | -16.42382023 |

As with the call the animation below shows the evolution of the trade.

Notice that even though the trader was delta hedged, the trade still lost money, although, not as much if it were not hedged. This means that delta hedging does not remove the time-decay element of options trading.

Dynamic Delta Hedging

Note that in the two examples above, even though the delta for the options was changing dynamically, the futures delta remained fixed at -0.53 for the call and 0.48 for the put, this is known as static delta hedging. It is also possible to dynamically adjust the futures position to take in to account the change in delta. Perhaps we may revisit this topic in a later article.

Summary

In this article we have described a technique called static delta hedging and how it applies to trading crypto options. Below are some pros and cons traders should be aware of when delta hedging.

Pros of Delta Hedging Options:

-

Risk Mitigation: Delta hedging helps mitigate the risk associated with changes in the price of the underlying asset. By adjusting the position in the underlying asset, the delta hedger can offset potential losses and protect the portfolio from adverse price movements.

-

Flexibility: Delta hedging allows investors to adapt their positions based on market conditions. They can adjust their hedge ratios and rebalance their portfolios to maintain a desired risk profile.

-

Reduced Cost: Delta hedging can help reduce the cost of holding options. By actively managing the hedge, investors can potentially offset some or all of the premium paid for the option, minimizing the overall cost of the position.

Cons of Delta Hedging Options:

-

Complexity: Delta hedging involves actively managing positions and continuously rebalancing the portfolio. This can be complex and time-consuming, requiring ongoing monitoring and adjustments.

-

Transaction Costs: Frequent adjustments to the delta hedge can lead to increased transaction costs, including brokerage fees and bid-ask spreads. These costs can eat into potential profits and impact overall returns.

-

Imperfect Hedge: Delta hedging provides protection against small price changes in the underlying asset. However, it does not eliminate all risks, especially in cases of large and sudden price movements. Delta hedging is based on the assumption of a linear relationship between the option's price and the underlying asset's price, which may not always hold true.